Joint Ventures in the UAE: What Every Foreign Investor Should Know Before Signing

May 2026

For decades, the joint venture was the price of entry to the UAE market. Foreign investors who wanted to trade onshore had little choice but to find a local partner, because the law required a UAE national to hold at least 51% of any mainland company. That world has changed. Since the 2020 reforms — most recently consolidated and extended under the amended Commercial Companies Law — foreign investors can now own 100% of a mainland company across most commercial, professional, and industrial activities, without a local shareholder and without a local service agent.

So a fair question is: if you no longer need a local partner, why are joint ventures still so common?

The answer is that the JV has quietly shifted from a legal obligation to a commercial strategy. Investors now enter joint ventures because they want to — to access local market knowledge, distribution networks, regulatory relationships, and shared risk that independent entry simply cannot replicate. But that shift carries a hidden danger. A JV entered into freely, as a matter of choice, tends to be treated more casually than one forced by law — and casual joint ventures are precisely the ones that end in expensive disputes.

This article sets out what every foreign investor should understand before signing a UAE joint venture: how to choose the right structure, where ventures most often break down, and the clauses that decide whether a partnership protects your investment or quietly exposes it.

First, Decide What Kind of Joint Venture You Are Building

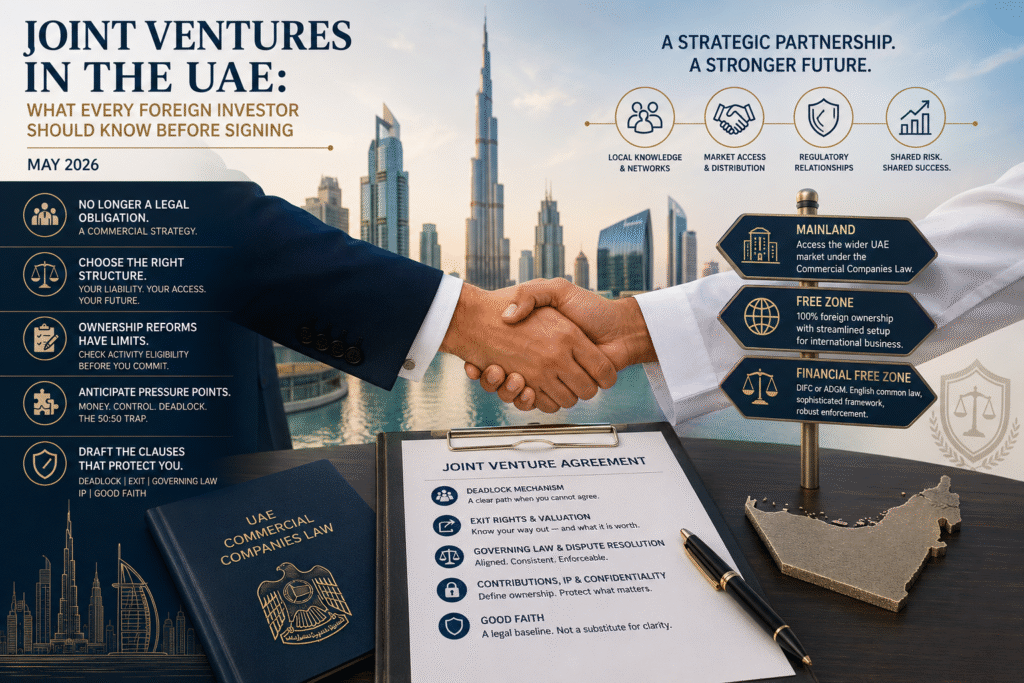

There is no single thing called a “joint venture” under UAE law. The term covers several quite different arrangements, and the first and most consequential decision an investor makes is which one to use.

A contractual (unincorporated) joint venture is created purely by agreement between the parties, without forming a separate legal entity. It is flexible, quick to set up, and well suited to a single project or a defined collaboration. But flexibility comes at a cost: in many unincorporated arrangements, particularly in construction, the partners can be jointly and severally liable to the client for performance — meaning each partner may be held responsible for the full extent of the obligations, regardless of how risk was divided internally. The internal indemnities you agree with your partner protect you against each other; they do not protect you against the outside world.

An incorporated (entity-based) joint venture creates a new company — most often a limited liability company — owned by the partners. This is the more durable structure for an ongoing business. It gives the venture its own legal personality, its own liability shield, and a clear framework for governance and ownership. The trade-off is that the company is then governed by the Commercial Companies Law and by its registered Memorandum of Association, which constrains what the partners can privately agree.

Layered on top of the entity choice is the jurisdictional choice, and for a foreign investor this matters enormously:

- A mainland JV falls under the federal Commercial Companies Law and is the right home for a business that needs to trade across the wider UAE market.

- A free zone JV offers 100% foreign ownership and streamlined setup, but typically confines the venture’s activities to within the free zone or to international business, rather than the onshore UAE market.

- A financial free zone — the Dubai International Financial Centre (DIFC) or the Abu Dhabi Global Market (ADGM) — applies an English common-law framework and offers more sophisticated corporate governance and a court system many international investors find familiar. For complex, high-value, or cross-border ventures, this can make shareholder rights significantly easier to enforce.

The structure is not an administrative detail to be settled after the commercial terms are agreed. It is itself a commercial decision — it determines your liability, your tax position, your access to the market, and how readily you can enforce the deal if it sours.

The Ownership Reform Has Not Removed Every Local-Partner Requirement

It is tempting to read “100% foreign ownership” as a blanket rule. It is not. The reforms removed the mandatory majority-Emirati shareholding for most activities — but the law expressly reserves a category of activities of strategic impact, determined by the Cabinet, where foreign ownership may still be restricted or made subject to specific licensing conditions. Sectors such as energy, defence, and certain telecommunications and security-related activities continue to attract local-partner or special-approval requirements.

For an investor, the practical lesson is that ownership rights are determined by how the business is licensed, not by nationality in the abstract. Before you assume you can own the venture outright, the activity must be checked against the relevant Department of Economic Development’s eligibility list, and the chosen legal form must be compatible with that activity. Misclassifying the activity at the outset is one of the most common — and most avoidable — ways to delay a licence or unexpectedly trigger an ownership restriction.

Where Joint Ventures Actually Break Down

Most JV disputes do not stem from bad faith. They stem from optimism at the outset — partners who get along well, share a vision, and quietly assume that the goodwill of the early days will carry them through every future disagreement. It rarely does. Four pressure points account for the majority of failures.

Money in, money out. The agreement must state precisely how capital is contributed, how ongoing costs are shared, what happens when the venture needs additional funding, and how and when profits are distributed. A partner who expected annual dividends and a partner who expected profits reinvested for growth can each be acting in perfect good faith and still be on a collision course. Disputes cluster around unclear contribution mechanisms and unplanned capital calls more than almost anything else.

Control and the things no one can do alone. Governance provisions set out voting rights, board composition, and decision-making thresholds. The most important of these are the “reserved matters” — the decisions (taking on debt, changing the business, admitting new shareholders, selling assets) that require the agreement of both partners rather than a simple majority. Define these too narrowly and a majority partner can reshape the venture over the other’s objection; define them too broadly and you create the conditions for paralysis.

The 50:50 trap. Equal ownership feels fair, and between a foreign investor and a local partner it is extremely common. But a 50:50 structure with no mechanism to break a tie is a dispute waiting to happen. When the partners disagree on a material decision, neither has the votes to prevail, and the venture simply freezes. Equal ownership signals equal commitment — but commitment is not a decision-making procedure.

The template that does not fit. Foreign investors frequently arrive with a shareholders’ agreement drafted for their home jurisdiction and assume it will work here. It often will not. UAE law has its own rules on pre-emption rights, share transfers, and penalty clauses, and — critically — UAE courts give precedence to the registered Memorandum of Association over a private shareholders’ agreement where the two conflict. An elegant English- or US-style agreement that contradicts the registered MOA may be worth far less than the investor believes at the moment they most need to rely on it.

The Clauses That Decide Your Fate

If money and control are where ventures break down, the following clauses determine whether a breakdown is survivable or catastrophic. These are the provisions a foreign investor should never leave to be “agreed later.”

A real deadlock mechanism

Every JV with shared control needs a pre-agreed answer to the question: what happens when we cannot agree? A workable mechanism defines clearly what counts as a deadlock, then sets out a structured escalation — typically a cooling-off period, referral to the senior executives of each partner, mediation, and, if all else fails, a binding resolution route. The blunt commercial backstops are the buy-sell mechanisms — arrangements (sometimes called “Russian roulette” or “Texas shoot-out”) that force one partner to buy out the other so the venture can continue under single ownership rather than dying in stalemate. An ambiguous deadlock clause is worse than none, because it gives each side a different reading to litigate over.

Exit rights — and an agreed way to value the exit

Investors spend enormous energy on how to get into a venture and almost none on how to get out. Yet the exit terms are where value is won or lost. A robust agreement should include a clear set of transfer controls: a right of first refusal so a partner cannot sell to a stranger without offering you the shares first; tag-along rights so a minority partner can join a sale on the same terms rather than being left behind with a new and unwanted majority owner; and drag-along rights so a majority can deliver a clean sale to a buyer who wants the whole company.

None of these mechanisms works, however, unless the parties have agreed in advance how the shares will be valued at the point of exit — whether by a fixed formula, an independent expert, or a named accounting firm conducting a fair-market valuation. Leaving valuation to be settled at the moment of exit, when interests are diametrically opposed, is one of the most reliable ways to turn a planned separation into litigation. It should never be treated as a detail to resolve later.

Governing law and dispute resolution

Because UAE joint ventures often bring together parties from different countries, the choice of governing law and dispute forum is not boilerplate — it is one of the most consequential clauses in the agreement. A UAE JV may elect to be governed by UAE federal law, by DIFC law, or by ADGM law, each offering a different default framework and judicial environment. Arbitration is the preferred route for many cross-border ventures, valued for its confidentiality and enforceability, with the Dubai International Arbitration Centre (DIAC) and the ADGM Arbitration Centre being the leading regional seats.

Whatever you choose, the dispute resolution clause must be aligned with the deadlock, exit, and governance provisions — and consistent across every document in the deal. Contradictory dispute and escalation provisions scattered across the MOA, the shareholders’ agreement, and side letters are a gift to a partner looking to delay and obstruct.

Contributions, IP, and confidentiality

Where partners contribute more than cash — assets, intellectual property, technology, or know-how — every contribution must be clearly valued and documented at the outset. Foreign investors who bring valuable IP into a venture should be especially careful to define who owns the IP that existed before the venture and who owns the IP created within it, and to back that with robust confidentiality protections. The know-how that made you an attractive partner is also the thing most easily lost if ownership and licensing are left vague.

Good faith is now a baseline obligation

One development deserves particular emphasis given recent reforms to UAE civil law: the legal expectation of good faith has been strengthened, and now reaches into the conduct of parties even before and around the formal contract. Partners in a UAE venture are expected to deal honestly and cooperatively in pursuing the venture’s objectives. This raises the legal stakes for a partner who withholds material information or behaves obstructively — but it is a backstop, not a substitute for clear drafting. Good faith fills gaps; it does not rewrite a badly structured deal in your favour.

How We Can Help

A joint venture is only as strong as the agreement underpinning it. Our corporate and commercial team advises foreign investors at every stage of a UAE joint venture — selecting and structuring the right entity and jurisdiction, confirming ownership and licensing eligibility, negotiating and localising shareholders’ and JV agreements, and building governance, deadlock, and exit mechanisms that hold up when they are tested. Where a venture has already run into difficulty, we act on shareholder and JV disputes, from deadlock and buy-out negotiations through to arbitration and litigation.

If you are entering the UAE market, forming a new venture, or reviewing an existing partnership, contact us for advice tailored to your circumstances — before you sign, not after.

This article is intended as general legal commentary and does not constitute legal advice. It reflects the law as at May 2026. For further information, please contact

Ahmed Hadeed

a.hadeed@hadeedpartners.ae

© Hadeed & Partners 2026